As September kicks off, European markets closed flat on the first trading day, reflecting a cautious mood among investors who are carefully assessing economic signals and market conditions. With the US financial markets closed for Labour Day, focus shifted to Europe and Asia, where mixed manufacturing data and corporate developments shaped market sentiment. In Europe, the pan-European Stoxx 600 saw little change, with gains in telecoms and certain tech stocks offset by declines in retail and manufacturing sectors. Meanwhile, Asian markets exhibited a mixed response to China’s latest economic data, highlighting ongoing concerns over global economic stability and growth prospects. As investors digest these developments, the global market landscape remains marked by uncertainty and divergent economic trends.

Key Takeaways:

- European Markets Close Flat on Mixed Sector Performance: The pan-European Stoxx 600 index closed slightly down by 0.04% on the first trading day of September, reflecting a cautious sentiment among investors. The performance across sectors was mixed, with retail stocks falling by 0.77% amid concerns over economic outlook and potential rate hikes. Conversely, telecom stocks saw a gain of 0.78%, lifted by positive corporate updates. The FTSE 100 Index declined by 12.79 points, or 0.15%, to end at 8,363.84, while the CAC 40 reversed early losses to close 0.2% higher at 7,646, driven by strong gains in pharmaceutical giant Sanofi, which surged 3.6% following a positive update on its multiple sclerosis treatments. Other contributors to the CAC 40’s rise included Orange, which gained 1.7%, and Unibail-Rodamco-Westfield, up 2.2%, although these were partially offset by declines in major companies such as Airbus (-1.4%), Stellantis (-0.8%), and Thales (-2.4%).

- Mixed Manufacturing Data Across Europe: Manufacturing data across Europe painted a varied picture, reflecting differing economic conditions among countries. The euro zone manufacturing PMI remained firmly in contraction territory at 45.8 in August, indicating a continued slowdown in manufacturing activity, primarily weighed down by declines in Germany and France. Germany’s manufacturing PMI fell to 42.4, the lowest in recent months, as a steep drop in incoming orders dampened hopes for a quick recovery in Europe’s largest economy. Meanwhile, France’s manufacturing sector also contracted at its fastest pace since January, with its PMI slipping to 43.9. However, the UK reported a positive uptick in manufacturing activity, with its PMI rising to 52.5, a 26-month high.

- Asian Markets React to Weak Chinese Data: Asian markets were mixed on Monday as investors digested weaker-than-expected economic data from China. The Hang Seng Index in Hong Kong dropped significantly by 1.85% in its final hour of trading, while the CSI 300 Index fell 1.70% to 3,265.01, marking its lowest point in seven months. The declines were largely driven by China’s manufacturing PMI, which fell to 49.1 in August, indicating a faster rate of contraction than the previous month and marking the fourth consecutive month of decline. This was below both July’s figure of 49.4 and economists’ median forecast of 49.5. Meanwhile, China’s non-manufacturing PMI showed a slight improvement, rising to 50.3 from July’s 50.2, but the modest increase did little to relieve concerns over the broader economic slowdown. The mixed data from China added to investor caution across Asia, with market participants closely watching upcoming economic reports from major regional economies, including South Korea’s inflation data and Australia’s second-quarter GDP.

- Oil Prices Edge Higher Amid Libyan Export Halt: Oil prices saw a modest recovery on Monday as geopolitical tensions and supply disruptions in Libya influenced market dynamics. Brent crude futures rose by 0.8% to settle at $77.52 per barrel, while U.S. West Texas Intermediate crude increased by 0.7% to $74.04 per barrel. The price gains followed reports of halted oil exports at major Libyan ports and production cuts across the country due to political unrest. The halted Libyan exports come amid expectations of increased oil supply from OPEC+ starting in October, creating a complex backdrop for oil traders. Analysts suggest that while the disruptions in Libya could temporarily support prices, the market remains wary of potential increases in supply from other OPEC+ members.

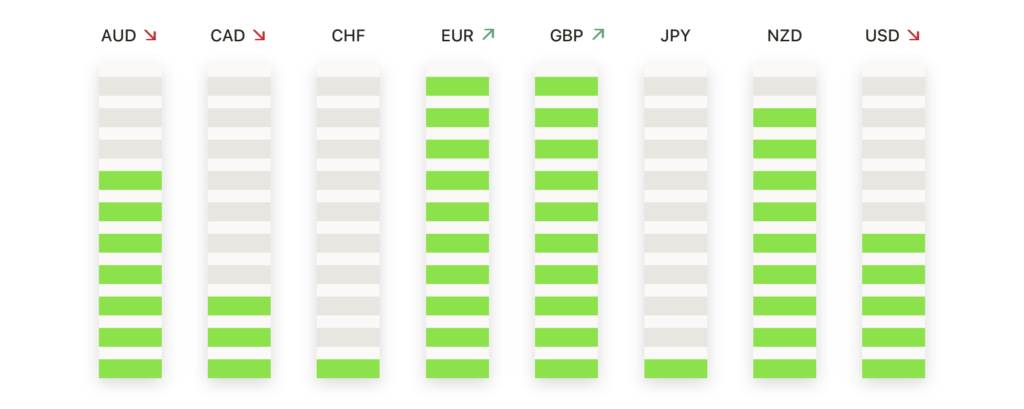

FX Today:

- EUR/USD Rebounds Amid USD Weakness: The EUR/USD pair started the week on a positive note, rebounding to the 1.1075 region after three consecutive days of losses. The pair benefited from a bit of selling pressure in the US Dollar, finding support near the 1.1050 level, which aligns with the 61.8% Fibonacci retracement of the August rally. As the EUR/USD attempts to regain higher ground, traders are eyeing resistance at the 2024 high of 1.1200, followed by the 2023 top of 1.1275. Key support levels to watch include the provisional 55-day SMA at 1.0898 and the crucial 200-day SMA at 1.0853.

- GBP/USD Starts September with Minimal Gains: The GBP/USD pair edged slightly higher on the first trading day of September, trading around 1.3145, up over 0.20% during the North American session. With US financial markets closed for Labour Day, the session saw limited activity. From a technical perspective, the GBP/USD is consolidating within the 1.3140-1.3270 range ahead of key US economic data releases later this week, including the Nonfarm Payrolls report. A break above last Friday’s peak of 1.3199 could pave the way toward the year-to-date highs of 1.3266, while a dip below the August 29 swing low of 1.3109 might trigger a move towards the 50-day moving average at 1.2894.

- USD/CHF Edges Higher as Swiss Franc Gains: The USD/CHF pair saw a slight increase, trading at 0.8511, up 0.2% for the day, as the Swiss Franc gained strength amid a quiet trading session due to the US holiday. Investors are now turning their attention to upcoming Swiss economic data, particularly the inflation report expected to show a slight decline to 1.2% year-on-year in August from 1.3% in July. Key support levels for USD/CHF are at 0.8503 and 0.8492, while resistance lies at 0.8532 and 0.8550.

- AUD/USD Recovers on USD Weakness and Risk Sentiment: The AUD/USD pair managed to recover from Friday’s retracement, advancing towards the 0.6790 region as the US Dollar showed signs of weakness. Despite disappointing economic data from China, including a drop in the manufacturing PMI to 49.1, the Australian dollar found support as risk sentiment improved slightly. The pair is approaching resistance at the 0.6800 level, with further gains potentially targeting the August high of 0.6823. On the downside, initial support is seen at 0.6760, followed by 0.6740.

- EUR/GBP Attempts Recovery Amid Bearish Pressure: The EUR/GBP pair showed a mild recovery during Monday’s session, rising to 0.8433 before retreating back to the 0.8420 level as sellers regained control. The technical outlook remains bearish, with indicators suggesting further downside potential. However, the pair might trade sideways above the 0.8400 area in the near term, given the oversold conditions. Immediate support levels are at 0.8400 and 0.8380, while resistance is seen at 0.8430 and 0.8450.

- Gold Tests Support as Dollar Strength Weighs: Gold (XAU/USD) edged down, testing support at $2,500 on Monday, as the recent recovery in the US Dollar put pressure on the precious metal. The daily chart indicates persistent selling pressure, with gold posting lower highs and lower lows. However, technical indicators remain within positive levels, suggesting limited bearish potential for now. Key support levels for gold are at $2,489, $2,475, and $2,463, while resistance levels stand at $2,508, $2,520, and $2,532. Despite the downward pressure, gold continues to hold above all moving averages, providing dynamic support and indicating that the overall trend may still favour the bulls.

Market Movers:

- Rightmove Soars on Acquisition Speculation: Rightmove’s shares surged by an impressive 27% after reports emerged that Australian rival REA Group is considering a takeover bid for the U.K.-based real estate listings platform. The potential acquisition sparked significant investor interest, driving Rightmove to one of its best trading days in recent years.

- Sanofi Gains on Positive Clinical Update: Sanofi’s stock climbed 3.6% after the company provided a positive update on its ongoing trials for multiple sclerosis treatments. The encouraging news fuelled investor optimism about the pharmaceutical giant’s growth prospects in the biopharmaceutical sector, making it one of the top gainers on the CAC 40.

- Ulta Beauty Falls on Lowered Sales Forecast: Ulta Beauty shares fell by more than 4% to lead declines in the S&P 500 after the company reported Q2 net sales of $2.55 billion, missing the consensus estimate of $2.61 billion. Additionally, Ulta lowered its 2025 net sales forecast to $11.0 billion-$11.2 billion from a previous forecast of $11.5 billion-$11.6 billion, below the consensus of $11.51 billion, contributing to the stock’s decline.

- New World Development Sinks on Loss Forecast: Shares of New World Development plunged as much as 14.14% after the Hong Kong-based property developer forecast a significant loss of about 19 to 20 billion Hong Kong dollars ($2.6 billion) for its financial year 2024. The dismal outlook spurred a strong negative reaction from investors, making it one of the biggest losers in the Asia-Pacific market.

- Crowdstrike Holdings Rises on Upgrade: Crowdstrike Holdings’ stock rose by more than 2% after HSBC upgraded the stock from ‘hold’ to ‘buy’ and set a new price target of $339. The upgrade reflected confidence in the company’s growth potential in the cybersecurity sector, driving investor interest higher.

As September begins, the global markets display a mix of caution and hope, reflecting the complex economic landscape investors are navigating. In Europe, the flat closing of the Stoxx 600, despite strong gains in certain sectors like telecoms and real estate, underscores the market’s wary stance amid mixed economic signals. Meanwhile, in Asia, weaker-than-expected manufacturing data from China has contributed to a more subdued market tone, with notable declines in key indices such as the Hang Seng and CSI 300. As investors digest these developments and look ahead to crucial economic data later this week, the markets remain poised between the forces of recovery and ongoing uncertainty.