Markets closed the week on a positive note, with the Dow Jones Industrial Average reaching a new all-time high and the S&P 500 notching its fourth consecutive month of gains. Investor optimism was fuelled by easing inflation data, including the US Personal Consumption Expenditures (PCE) price index, which suggested a steady inflationary environment and boosted hopes for potential rate cuts by central banks. Strong performances in technology stocks and encouraging earnings reports added to the upbeat sentiment, even as oil prices slipped due to anticipated increases in supply. As traders digest these mixed signals, the focus remains on upcoming central bank decisions and key economic indicators that could shape the next phase of market movements.

Key Takeaways:

- Dow Jones Hits Fresh Record High: The Dow Jones Industrial Average rose 0.55%, adding 228.03 points to close at a new all-time high of 41,563.08. This increase capped off a strong end to a volatile month, reflecting renewed investor optimism.

- S&P 500 Marks Fourth Consecutive Winning Month: The S&P 500 advanced 1.01% to close at 5,648.40, recording a 2.3% gain for August. This marks the fourth straight month of gains for the index, lifted by strong performances in consumer staples, real estate, and healthcare sectors.

- Nasdaq Composite Climbs on Tech Strength: The tech-heavy Nasdaq Composite gained 1.13% to finish at 17,713.62. Despite a challenging start to the month, the index managed to secure a 0.7% rise for August, driven by robust investor interest in technology stocks.

- European Stocks Close August at Record Highs: The pan-European Stoxx 600 reached an intraday record high of 526.66 points before closing above 525 points for the first time, ending August 1.3% higher. This recovery was strengthened by a decline in eurozone inflation to a three-year low of 2.2%, supporting expectations of a September rate cut by the European Central Bank. Major indexes like the FTSE 100 and CAC 40 also posted gains, rising 0.10% and 0.79%, respectively, as investors welcomed easing inflationary pressures.

- Asia-Pacific Markets Rebound Amid Positive US Data: Asian markets experienced a notable uptick, with Hong Kong’s Hang Seng index climbing 1.44% and Japan’s Nikkei 225 rising 0.74% to 38,647.75, its highest since late July. Stronger inflation figures from Tokyo and a surge in retail sales, alongside calming US economic data, helped alleviate recession fears and prompted a positive response across the region. Australia’s S&P/ASX 200 also gained 0.58%, nearing its all-time high, reflecting broad regional strength.

- Oil Prices Fall Amid Supply Concerns: Oil prices declined as investors anticipated an increase in OPEC+ supply starting in October. US West Texas Intermediate crude futures dropped 3.11% to $73.55 per barrel, and Brent crude futures fell 1.43% to $78.80 per barrel. The prospect of higher output from the oil cartel, coupled with persistent uncertainty around US interest rate cuts, weighed on the energy market, contributing to a 2.4% decline in Brent crude prices for the month.

- Fed’s Preferred Inflation Gauge Matches Expectations: The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred measure of inflation, rose 0.2% in July and 2.5% year-over-year, aligning with economists’ expectations. The core PCE, which strips out food and energy costs, also increased by 0.2% from the previous month, supporting a stable inflation outlook that may influence the Fed’s upcoming policy decisions.

- Treasury Yields Rise Following Inflation Data: US Treasury yields moved higher as investors digested the latest inflation data, with the 10-year note rising nearly 6 basis points to 3.909% and the 2-year yield increasing nearly 4 basis points to 3.919%. The rise in yields reflects market expectations of future rate decisions by the Federal Reserve amid ongoing economic assessments.

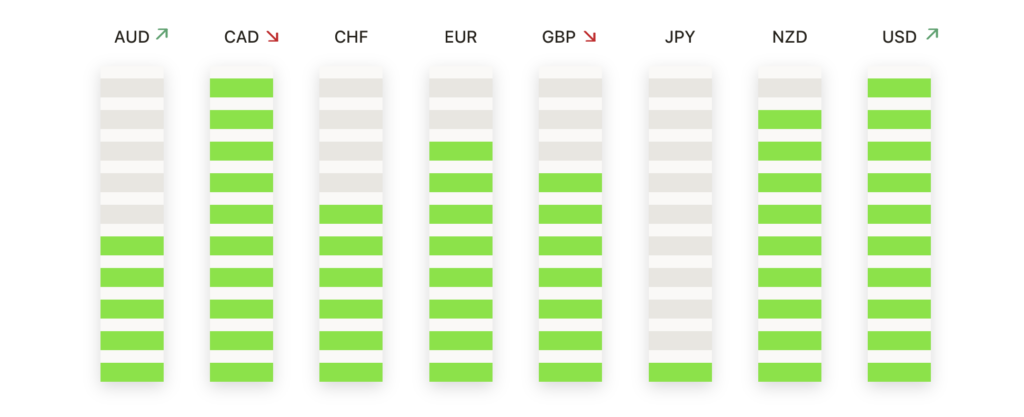

FX Today:

- Gold Around $2,500 as Treasury Yields Rise: Gold prices tumbled by over 0.70% on Friday, closing at the $2,503 mark for the second consecutive day at $2,497. The decline was driven by stronger US Treasury yields, with the 10-year note yield rising by 4.5 basis points to 3.909% following the release of the US core Personal Consumption Expenditures (PCE) Price Index. If XAU/USD trades below $2,500, the next support level to watch is the August 22 low of $2,470. A break below this could see further declines toward the 50-day Simple Moving Average (SMA) at $2,431. On the upside, if gold manages to stay above $2,500, resistance could be seen at $2,550, with a potential move towards $2,600 if bullish momentum resumes.

- EUR/USD Slumps as Market Awaits Fed Decision: The EUR/USD pair extended its downward slide on Friday, falling to 1.1045 as traders reacted to mixed economic signals. Despite eurozone inflation dropping to a three-year low of 2.2% in August, the data failed to provide support to the euro, which remained under pressure from a stronger US Dollar. The pair has now declined for three consecutive days, moving closer to the 50-day Exponential Moving Average (EMA) at 1.0950. Although EUR/USD remains above the 200-day EMA at 1.0855, the loss of upward momentum suggests further declines could be in store if market sentiment does not improve.

- GBP/USD Remains Under Pressure: The GBP/USD pair struggled to gain traction on Friday, trading around 1.3130 as the US Dollar held firm following the latest inflation data. Despite attempts to break above 1.3200, the pound remained in negative territory, unable to mount a significant recovery. The pair’s near-term outlook remains bearish, with key support at the psychological level of 1.3000. However, the longer-term technical setup shows that GBP/USD is still holding above its upward-sloping 20-week Exponential Moving Average (EMA) near 1.3000, suggesting potential for a rebound if market conditions improve. On the upside, resistance is seen at 1.3500 and the February 2022 high of 1.3640 if bullish momentum builds.

- AUD/USD Declines on Stronger US Dollar: The AUD/USD pair fell by 0.53% to 0.6762 on Friday, as the US Dollar strengthened following the release of July’s Personal Consumption Expenditures (PCE) figures. The Australian dollar, despite support from the Reserve Bank of Australia’s hawkish stance, could not withstand the broad-based dollar rally. The Relative Strength Index (RSI) is currently at 58, pointing downwards, indicating that selling pressure is mounting. The Moving Average Convergence Divergence (MACD) shows flat green bars, suggesting that the bullish momentum seen earlier may be fading. Key support levels to monitor are 0.6750 and 0.6730, while resistance levels are positioned at 0.6800 and 0.6830.

- USD/JPY Rallies as Yields Support Dollar: The USD/JPY pair surged past the 146.00 level for the first time this week, closing at 146.17 on Friday. The 10-year Treasury note yield increased, underpinning the dollar’s strength against the yen. Despite the upward move, the pair faces key resistance levels at 146.93 and 148.46. A failure to break above these levels could see the pair retrace towards 145.39, with potential for further declines towards the August 26 low of 143.44 if bearish sentiment re-emerges.

Market Movers:

- Intel Surges on Strategic Business Review: Intel shares jumped 9.5% after news broke that the company is working with bankers to explore options to address weaknesses in its core business. This development has sparked optimism among investors about potential strategic moves to enhance Intel’s market position, driving its stock price higher.

- Elastic NV Plummets on Disappointing Revenue Forecast: Elastic NV saw its shares plunge by 26.5% after the company’s fiscal second-quarter revenue forecast missed Wall Street expectations. The artificial intelligence search company now projects revenue between $353 million and $355 million, falling short of the $361 million estimate.

- MongoDB Soars on Earnings and Revenue Beat: MongoDB shares surged over 18% following a strong second-quarter earnings report. The company posted an earnings per share of 70 cents, excluding items, on revenue of $478 million, significantly beating the 49 cents per share and $464 million in revenue expected by analysts. MongoDB also provided an optimistic third-quarter revenue forecast, expecting between $493 million and $497 million, well above the analyst estimate of $479 million.

- Marvell Technology Gains on Strong Forecast: Marvell Technology’s stock climbed over 9% after the company released an upbeat third-quarter forecast. Marvell expects adjusted earnings of 40 cents per share on revenue of $1.45 billion, surpassing the consensus estimate of 38 cents per share and $1.40 billion in revenue. This positive outlook has boosted investor confidence in the company’s growth prospects.

- Alibaba Rises as Regulatory Oversight Concludes: Alibaba’s US-traded shares increased nearly 3% after China’s market regulator announced the completion of a three-year oversight process. This marks a significant milestone for Alibaba, which was fined by the regulator in 2021 as part of an antitrust investigation. The conclusion of regulatory scrutiny has alleviated some of the pressures on the company, contributing to the positive market response.

- Dell Climbs on Earnings Beat and Strong Guidance: Dell shares rose more than 4% after the company reported better-than-expected earnings and revenue for the second quarter. Dell’s positive performance was complemented by its guidance for the current quarter, which aligns with market expectations, further boosting investor sentiment.

As August unfolds, global markets showed resilience, with major indexes like the Dow Jones, S&P 500, and Nasdaq Composite closing higher, reflecting a renewed sense of optimism despite a volatile month. Strong performances from technology and healthcare sectors, coupled with easing inflation data in both the US and eurozone, provided a solid foundation for investor confidence. While the US Dollar gained strength against other currencies and oil prices fell on supply concerns, market participants continue to navigate a complex landscape marked by economic data and central bank policies. As September approaches, all eyes will be on the Federal Reserve and European Central Bank for further cues on interest rates and economic support, setting the stage for the next phase in this dynamic market environment.