Monday’s trading session on Wall Street saw a mixed performance, with the major indexes struggling to find clear direction as investors prepared for pivotal economic data later this week. The S&P 500 remained flat while the Nasdaq Composite gained, boosted by a 4% surge in Nvidia shares. The Dow Jones Industrial Average, however, dipped by 140 points, reflecting a cautious market sentiment. As traders awaited the upcoming Consumer Price Index (CPI) report, which is expected to provide crucial insights into the health of the US economy, global markets also struggled with mixed outcomes. European stocks closed with minor fluctuations, while Asia-Pacific markets showed signs of recovery following a volatile week. All eyes are now on the forthcoming inflation data, which could set the tone for market movements in the coming days.

Key Takeaways:

- S&P 500 Ends Flat Amid Volatility: The S&P 500 finished Monday’s session essentially unchanged, closing at 5,344.39 with a negligible gain of 0.23 points. Throughout the day, the index wavered between slight gains and losses, mirroring the cautious sentiment among investors who are bracing for key economic data later this week. This lack of decisive movement underscores the market’s sensitivity to upcoming reports.

- Nasdaq Rises on Tech Strength: The Nasdaq Composite advanced 0.21% to close at 16,780.61. This gain highlights the continued strength in the technology sector, which remains a focal point for investors amid broader market uncertainty. The Nasdaq’s performance indicates ongoing confidence in the tech-heavy index.

- Dow Jones Retreats Amid Investor Caution: The Dow Jones Industrial Average declined by 140 points, or 0.36%, ending the day at 39,357.01. This pullback reflects investors who are treading carefully as they await the CPI report. The Dow’s decline, despite resilience in other major indexes, suggests a divergence in market sentiment, with some sectors experiencing more pressure than others.

- European Markets Mixed with Focus on BT Group Acquisition: European stocks ended Monday’s session with mixed results, as the pan-European Stoxx 600 index remained flat while the FTSE 100 rose by 42.15 points, or 0.52%. The slight gains in the FTSE 100 contrast with the broader European market’s hesitation, reflecting uncertainty as investors anticipate US and UK inflation data later this week. Notably, BT Group shares jumped 8.43% after Bharti Enterprises’ international investment arm announced plans to acquire a 24.5% stake in the company, valued at approximately £3.2 billion. This move has sparked significant interest in the telecommunications sector, contributing to the overall mixed performance of European markets.

- Asia-Pacific Markets Show Resilience Despite Volatility: In the Asia-Pacific region, markets mostly rose after a mixed week, with South Korea’s Kospi climbing 1.15% to close at 2,618.30 and Australia’s S&P/ASX 200 advancing 0.46% to 7,813.7. These gains suggest a degree of recovery following last week’s sell-offs, although Mainland China’s CSI 300 index slipped by 0.17% to 3,325.86, indicating that not all markets are fully out of the woods. Meanwhile, Japan markets were closed for a holiday.

- US Treasury Yields Decline as Inflation Data Looms: Yields on US Treasury bonds dipped on Monday, with the 10-year yield falling by 3.7 basis points to 3.905% and the 2-year yield dropping by 3.8 basis points to 4.015%. This decline in yields reflects investor anticipation of the upcoming inflation data, which could significantly influence Federal Reserve policy. The movement in yields suggests a flight to safety as market participants seek to hedge against potential volatility in response to the forthcoming economic reports.

- Three-Year Inflation Expectations Hit Record Low: The latest New York Federal Reserve survey revealed a record low in three-year inflation expectations, which fell to 2.3% in July, down 0.6 percentage points from June. This marks the lowest level since the survey’s inception in June 2013. While short-term inflation expectations remain elevated at 3%, the significant drop in the three-year outlook suggests growing consumer confidence that inflation will moderate over the longer term. This development comes at a crucial time, with the Federal Reserve closely monitoring inflation expectations as it considers future interest rate adjustments.

- Budget Deficit Jumps in July: The US federal budget deficit surged in July, reaching over $1.5 trillion for the year as monthly shortfalls grew by $243.7 billion. This increase was driven by a significant rise in Medicare expenses, which soared to $92 billion for the month, and elevated net interest payments, which totalled $81 billion. The expanding deficit highlights the growing fiscal challenges facing the US government, particularly as it deals with high interest rates and increased spending on entitlement programs. The growing deficit has also contributed to pushing the federal debt to a staggering $35.1 trillion.

FX Today:

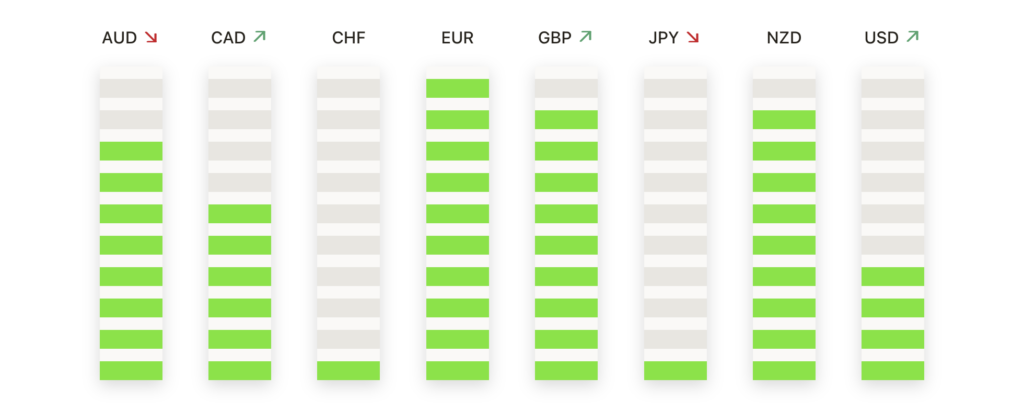

- EUR/USD Rises Amid US Data Anticipation: The EUR/USD pair gained 0.14% on Monday, closing at 1.0930 after peaking at 1.0940 during the session. The pair is currently capped by resistance at 1.1008, while support is anchored at the 200-day SMA of 1.0834. A drop towards 1.0777 could occur if selling pressure increases.

- Pound Steady in Narrow Range: GBP/USD remained largely unchanged, ending the day around 1.2770. Strong resistance is noted at 1.2800-1.2810, where critical technical levels converge. Should the pair dip below 1.2750, it might test support levels at 1.2700 and 1.2660.

- Yen Weakens After Brief Rally: USD/JPY touched a six-day high of 148.22 before retreating to close below 147.79. The pair faces significant resistance at 148.00, with key support at 146.27. Further declines could target the 145.44 level, while a break above 148.00 would aim for the 200-DMA at 151.46.

- Loonie Holds Firm as USD/CAD Struggles: USD/CAD encountered resistance at the 50-day EMA of 1.3740, softening slightly as it remains supported by the 200-day EMA at 1.3625. The pair’s inability to break higher suggests that a pullback towards 1.3550 may be on the horizon if the Canadian dollar strengthens.

- Gold Nears Record Highs: Gold prices surged over 1.5% on Monday, closing at $2,470 as it approaches the all-time high of $2,483. The metal found support at $2,450, with bullish momentum suggesting a potential test of the psychological $2,500 level. On the downside, key support lies at $2,400 should the rally lose steam.

Market Movers:

- JetBlue Plunges on Debt Concerns: JetBlue shares tumbled by more than 20% after the airline announced plans to sell $400 million in five-year convertible senior notes. The market reacted negatively to the increased debt load, with credit ratings agencies S&P Global, Moody’s, and Fitch downgrading the company’s outlook, citing concerns over its financial stability.

- Hawaiian Electric Drops on Massive Q2 Loss: Hawaiian Electric Industries saw its stock plummet by over 14% following the announcement of a $1.3 billion net loss in the second quarter, translating to a loss of $11.74 per share. This stark contrast to the $55.1 million net income reported in the same period last year, coupled with uncertainty surrounding a $1.7 billion settlement payment related to the Maui windstorm and wildfire, has significantly shaken investor confidence.

- KeyCorp Surges on Scotiabank Investment: KeyCorp shares soared by 9%, making it the top performer in the S&P 500 on Monday, after the Bank of Nova Scotia announced plans to acquire a 14.9% stake in the regional bank. The deal, valued at approximately $2.8 billion, will inject significant capital into KeyCorp, boosting investor sentiment and driving the stock higher.

- Monday.com Hits New High on Strong Q2 Earnings: Monday.com shares surged more than 14% to a new 52-week high after the Israel-based software company reported better-than-expected second-quarter results. The company posted earnings of 94 cents per share, significantly beating analyst expectations of 56 cents, with revenue reaching $236.1 million, surpassing the estimated $229 million.

- Marathon Digital Slumps on Debt Offering: Shares of Marathon Digital Holdings dropped by more than 11% after the cryptocurrency miner announced a $250 million private debt offering of seven-year notes. The market expressed concerns over the dilution of equity and the potential impact of increased debt on the company’s balance sheet.

- Starbucks Rises on Activist Investor Interest: Starbucks shares gained more than 2% following reports that activist investor Starboard Value, led by Jeff Smith, has acquired a stake in the coffee giant. The Wall Street Journal reported that Starboard is pushing for strategic changes to boost the stock price, which has sparked renewed investor interest in the company.

- Qualcomm Falls on Downgrade: Qualcomm shares declined by about 1% after downgraded the chipmaker to “peer perform” from “outperform.” The downgrade was driven by concerns over Apple’s decision to use its own internal modem, potentially reducing Qualcomm’s revenue from one of its largest clients.

As the week begins, the mixed performance across Wall Street and global markets highlights a cautious yet hopeful investor sentiment. With the S&P 500 remaining flat and the Nasdaq inching upward, driven by tech strength, the market’s attention is squarely focused on the upcoming US inflation data, which could significantly influence future market direction. European and Asia-Pacific markets reflect a similar tone, particularly as key economic reports loom large. The notable movements in individual stocks, from JetBlue’s sharp decline to KeyCorp’s rally, underscore the diverse factors at play, from corporate earnings to geopolitical tensions. Investors now await the mid-week economic reports, which are poised to either reinforce or challenge the prevailing market trends.