US stocks ended Monday broadly unchanged as traders turned their focus to a high-stakes week for central bank policy and consumer data. Market attention is firmly on Jerome Powell’s upcoming speech at the Jackson Hole symposium, expected to shape expectations for the Federal Reserve’s next policy move. Retail giants including Walmart, Target, Home Depot and Lowe’s are also due to report earnings, offering a key gauge of consumer spending strength as valuations remain stretched. Geopolitics also remained in focus as Donald Trump met with Ukrainian President Volodymyr Zelensky and European leaders in Washington, ahead of a planned call with Russia’s Vladimir Putin to explore a potential trilateral discussion. The mix of policy signals, earnings reports and global politics has left investors cautious, with momentum from recent gains now giving way to a wait-and-see approach.

Key Takeaways:

- Dow Edges Lower After Winning Streak: The Dow Jones Industrial Average slipped 34.30 points, or 0.08%, to 44,911.82 as traders paused following two consecutive weeks of gains. Losses in Meta and Microsoft weighed on sentiment, with Meta falling 2.3% and Microsoft down 0.6%.

- S&P 500 Flat as Momentum Cools: The S&P 500 ended little changed, down 0.01% at 6,449.15, as markets struggled to extend recent rallies. The index has advanced in 4 of the last 5 weeks.

- Nasdaq Holds Steady Amid Tech Weakness: The Nasdaq Composite inched higher by 0.03% to 21,629.77, managing to stay positive despite pressure from large-cap tech. Meta Platforms’ 2.3% decline and Microsoft’s 0.6% fall pulled on the broader index.

- European Markets Mixed as Leaders Meet Trump: European stocks were mixed as traders monitored both corporate news and meetings in Washington between Donald Trump, Volodymyr Zelensky and European leaders. The Stoxx 600 closed marginally higher, with healthcare stocks up 1.4% after Novo Nordisk surged 6.6% on fresh US approval for its Wegovy treatment. London’s FTSE 100 added 0.21% to 9,157.74, Portugal’s PSI 20 climbed 1.28% to 7,880.25, and Spain’s IBEX 35 slipped 0.17% to 15,251.69 despite its highest level since 2008. France’s CAC 40 dropped 0.53%, while Germany’s DAX fell 0.2% to 24,302 and Italy’s FTSE MIB was flat at 42,641. Germany reported a 7.9% year-on-year rise in June home building permits.

- Asia-Pacific Stocks Mostly Higher Ahead of Talks: Asian equities closed mostly stronger as investors watched for developments in US-Ukraine discussions. Japan’s Nikkei 225 rose 0.96% and the Topix added 0.7%. In South Korea, the Kospi fell 1.17% and the Kosdaq slipped 1.78%, though the Kospi remains up 32% year-to-date. Hong Kong’s Hang Seng gained 0.62%, while mainland China’s CSI 300 jumped 1.5% to its highest since October 2024. Taiwan’s Taiex rose 0.43%, India’s Nifty 50 climbed 1.35% and the Sensex added 0.89%. Australia’s S&P/ASX 200 ended 0.11% higher after briefly touching a record intra-day high, while Singapore reported non-oil domestic exports falling 4.6% in July, worse than expected, after a sharp 12.9% rise in June.

- Oil Prices Firm After Trump–Zelensky Talks: Crude oil edged higher after Trump and Zelensky met in Washington following Friday’s inconclusive US–Russia summit. Brent rose 1.00% to $66.51 a barrel, while WTI added 0.83% to $63.32. Traders weighed the risk of sanctions tightening against Russia with prospects for peace negotiations that could alter supply flows.

- Treasury Yields Edge Up Before Fed Minutes: US Treasury yields rose as investors awaited Wednesday’s release of July Fed minutes and Powell’s Jackson Hole remarks later in the week. The 2-year yield rose 1 basis point to 3.769% and the 10-year yield climbed to 4.339%. It was the first Fed meeting since 1993 where multiple governors dissented, choosing immediate rate cuts.

FX Today:

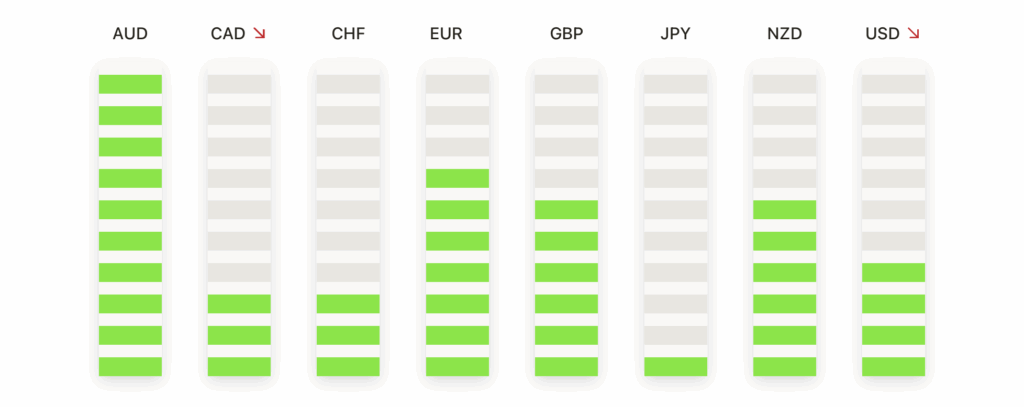

- EUR/USD Retreats as Resistance Holds Firm: EUR/USD closed at 1.1667, down 0.30% after trading between 1.1666 and 1.1712, with sellers regaining control following repeated failures to sustain traction above the 1.1700 mark. The daily candle printed a red body, reflecting fading momentum even as the pair held comfortably above the 50-day SMA at 1.1636. Broader trend dynamics remain constructive, with the euro still advancing from March’s trough near 1.0700, but near-term price action is locked between strong support at 1.1630 and overhead resistance at 1.1715. Structurally, this consolidation highlights hesitation after the strong rallies seen in June and July, with the 100-day SMA at 1.1453 and the 200-day at 1.0987 continuing to underpin the longer-term recovery. A confirmed push above 1.1715 would reassert bullish control and open the path to 1.1800, while a close beneath 1.1630 would weaken the structure and risk a deeper slide towards 1.1550.

- GBP/USD Pulls Back as Bulls Struggle: GBP/USD closed at 1.3507, down 0.33% after ranging between 1.3503 and 1.3555, with a red daily candle showing sellers regaining ground after last week’s rebound. The pair is hovering around the 50-day SMA at 1.3510, which has flattened, signalling hesitation near current levels, while the 100-day at 1.3400 and the 200-day at 1.3010 continue to provide a supportive base. Structurally, sterling has advanced from the August low near 1.3200, forming higher lows but stalling repeatedly around the 1.3550–1.3600 zone. Momentum has cooled, and the rejection near 1.3555 highlights fading short-term strength. Initial support lies at 1.3500 and deeper at 1.3400, where the 100-day average reinforces the bullish structure, while resistance stands at 1.3560 and then 1.3650, a ceiling that capped rallies through July. A break above 1.3560 would likely open the path to 1.3650, while sustained weakness below 1.3400 would undermine the bullish bias.

- USD/CHF Climbs Above Key Averages as Buyers Target 0.8850: USD/CHF closed at 0.8806, up 0.40% after trading between 0.8764 and 0.8815, with a strong green daily candle showing buyers regaining control. Price action moved back above the 50-day SMA at 0.8761, reinforcing short-term momentum alongside support from the 100-day SMA at 0.8725 and the 200-day at 0.8794. The broader structure has been in recovery since July’s low near 0.8600, with higher lows forming a medium-term base. The recent push above 0.8800 marks a critical step, though resistance remains near 0.8850, a level that capped several rallies last month. Immediate support lies at 0.8760 and 0.8725, with a deeper cushion at 0.8700.

- USD/JPY Rebounds Toward Resistance as Buyers Eye 148.00: USD/JPY settled at 147.83, gaining 0.49% after swinging between 147.08 and 147.99, with a solid green candle signalling renewed bullish momentum. The pair climbed back above the 50-day SMA at 146.52, supported by a bullish crossover against the 100-day SMA at 145.47. Price action remains within a broader consolidation range that has shaped trade since July, with buyers repeatedly defending the 146.00 floor while sellers cap upside near 149.00. Structurally, the 200-day SMA at 149.21 continues to act as a ceiling, keeping broader momentum in check despite the recovery from June’s lows. The market is now testing the midpoint of the summer range, with levels in focus at 148.00 and 149.00 on the topside, while support sits at 146.50 and 146.00 on the downside.

- Gold Holds Range as Buyers Defend Support: Gold closed at $3,334, slipping 0.04% after trading between $3,324 and $3,358, with a small-bodied daily candle reflecting muted momentum. Price remains anchored above the 100-day SMA at $3,299, with the 50-day at $3,348 and the 200-day at $3,031 maintaining a broadly supportive structure. Since peaking above $3,500 earlier this summer, the metal has entered consolidation, carving overlapping candles while defending higher bases compared with May. Structurally, gold is oscillating around the $3,330–$3,360 zone, with buyers repeatedly preventing deeper breakdowns despite tests of the 100-day average. The bias leans cautiously bullish while holding above the $3,300 handle, with resistance seen at $3,360 and then the July high at $3,440. On the downside, support rests at $3,324 and then $3,300.

Market Movers:

- Natural Gas Producers Sink on Sector Downgrade: EQT fell over 4%, Comstock lost more than 6% and Antero dropped over 5%, while Corterra and Range Resources slipped over 3% and Expand Energy more than 2% after Roth Capital cut the group on oversupply concerns.

- Intel Declines on Government Stake Talks: Intel slid more than 3% after reports the Trump administration is considering a 10% stake that would make Washington its largest shareholder.

- Meta Falls on AI Restructuring Plan: Meta dropped more than 2% after reports it is planning its fourth reorganisation of its artificial intelligence unit in six months.

- Northern Oil & Gas Weakens After Downgrade: Northern Oil & Gas slipped more than 2% after Morgan Stanley cut its rating to underweight from equal weight.

- Dayforce Soars on Takeover Speculation: Dayforce surged more than 25% to top the S&P 500 after reports of buyout talks with private equity group Thoma Bravo.

- Duolingo Rallies on New Buy Rating: Duolingo jumped over 12% after Citigroup initiated coverage with a buy recommendation and a $400 price target.

- EPAM Systems Gains on Analyst Upgrade: EPAM rose more than 4% after TD Cowen lifted its rating to buy from hold and set a $205 price target.

Markets began the week on a quiet note as investors balanced upcoming retail earnings, heightened geopolitical developments, and the looming Jackson Hole symposium. With rate expectations finely poised and valuations stretched, traders largely chose to hold positions, awaiting signals from Powell’s remarks and consumer-sector results. European and Asian markets provided mixed direction, reflecting both regional corporate news and the weight of international politics. Commodities and currencies showed consolidation rather than breakout moves, underscoring a cautious tone across asset classes. Attention now turns to central bank commentary and earnings data in the days ahead, which are likely to set the tone for market momentum into the final stretch of August.